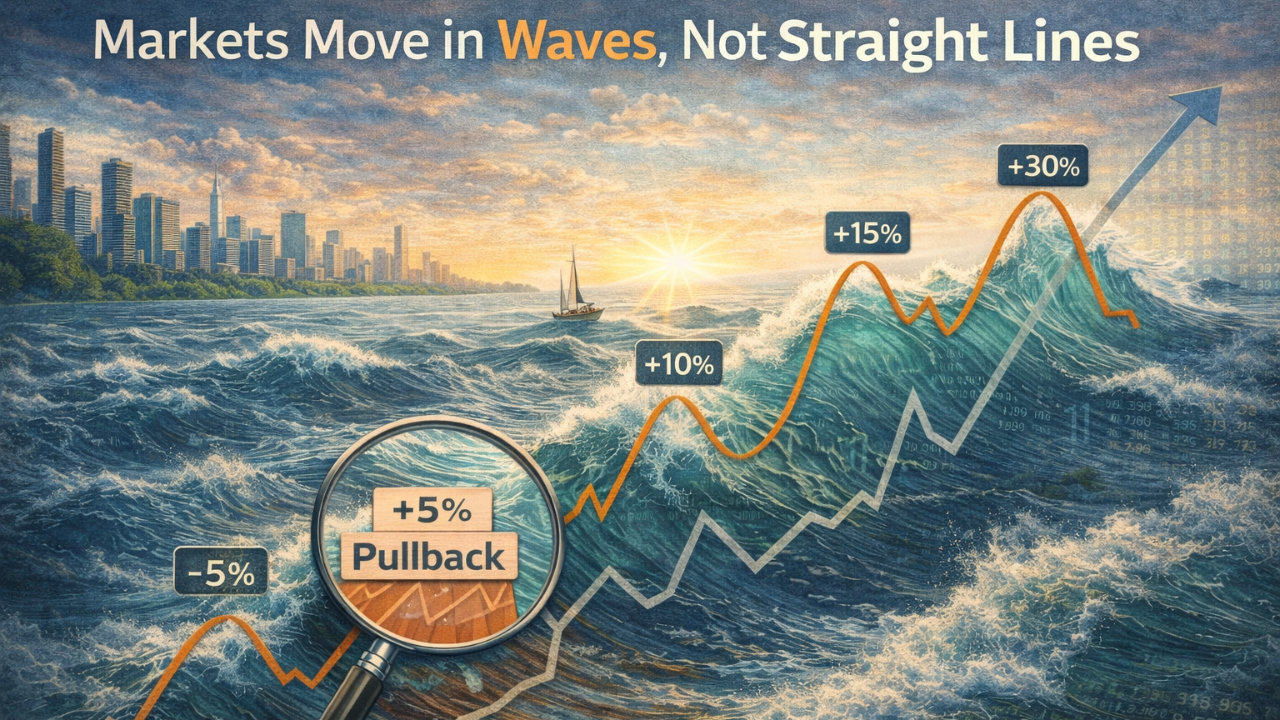

Client Memo: Markets Move in Waves, Not Straight Lines

Dec 01, 2025Over the past few days, you’ve likely seen headlines about the stock market “sliding,” “selling off,” or “pricing in an AI bubble.” Major U.S. indexes have pulled back a few percent from recent highs, and day-to-day swings have picked up again. As of this week, the S&P 500 is down a little 5% from its late-October peak, its largest pullback since the spring, and volatility indexes have moved to one-month highs.

This is not abnormal. The fact that we went nearly seven months without more than a 2.5% decline in the S&P 500 is the abnormality. Still, that can feel uncomfortable. Anytime we see long periods of low volatility and gains, any amount of decline can feel like the end of the world. But history is very clear on one point:

Pullbacks and corrections are a normal, recurring feature of bull markets – not a sign that long-term investors are “doing it wrong.”

Below is some perspective to help frame what’s happening now.

What’s Happening Now

A few themes are driving the recent swings:

- Valuation worries in technology and AI-related names. After a powerful run in a handful of mega-cap tech and AI companies, investors are reassessing how much they’re willing to pay for future growth. The key catalyst here was an interview with OpenAI (Chat GPT creator) Sam Altman where he ‘shut down’ a question on how a company that currently has $13B in revenue can commit to spending $1.4 trillion. This caused some investors to reassess the current prospects for earnings growth over the next five to ten years.

- Shifting expectations for Federal Reserve rate cuts. Investors came into the fall expecting a series of quick interest-rate cuts and the markets were priced for such. Following the recent Fed meeting where Powell threw cold water on a December cut, those odds have faded. With the market re-pricing interest rate cuts, stocks of the most rate-sensitive (including technology companies) and speculative areas have seen selling.

- A market that had gone unusually long without much volatility. After months of relatively smooth gains and fresh all-time highs in 2024 and mid-2025, a bout of downside volatility is more noticeable – but not unusual.

In other words, we’re seeing a normal reset in a market that had become stretched if we are discounting based on a higher interest rate. However, there is no clear evidence that the entire long-term bull market is over.

The Data: Volatility Is the Cost of Admission

Several long-term statistics are worth keeping in mind:

- Since 1980, the average intra-year decline (peak-to-trough drop at some point during the year) for the S&P 500 has been about 14%, even though most of those years finished positive.

- In one study of 45 years since 1980, the S&P 500 had a negative intra-year drawdown every single year, yet 34 of those 45 years still finished with gains.

- Looking back to 1990, the average drawdown in any calendar year has been about -13.7%; even in years when the market ultimately finished positive, the average drawdown was still roughly -8.3%.

- '5–10% pullbacks are “super common” – investors typically see one or more of these nearly every year. Declines of 15% are still common; 25%+ and true bear markets are much less frequent.

- Historically, a 10% correction (a drop from a high of at least 10%) has occurred about every 19–20 months on average going back to 1928. More recent data suggest roughly six out of ten years see at least one 10% correction.

The conclusion is simple:

You cannot get long-term stock returns without accepting regular, sometimes sharp, short-term declines. Even years that end up looking “calm” on a long-term chart usually involved a period that felt stressful in real time.

Why Volatility Can Be Healthy

As uncomfortable as it feels, these “air pockets” can actually improve the health of a bull market:

- They shake out speculation. Stocks and themes that ran too far, too fast often see the sharpest reversals. That can relieve pressure in the most expensive corners of the market and reduce bubble risk.

- They reset expectations. When investors start to assume every dip will be immediately bought and every earnings report will beat expectations, risk builds. Pullbacks force people to revisit assumptions about growth, rates and valuations.

- They create opportunities. High-quality companies can trade at more attractive prices after a pullback. For long-term investors, volatility is often when future returns are being “put on sale.”

- They remind investors of their time horizon. Episodes like this are a good reminder that if your goals are 5, 10 or 20+ years away, then what the market does over a few days or weeks is noise, not a thesis.

How We Think About the Next Few Months

No one knows if this particular pullback will stop at 3–5%, widen into a standard 10% correction, or reverse quickly. Nvidia is driving the market, and I waited for their third quarter results to come through before finishing. They look strong and the stock is up, which should put a floor under the market in general.

We could see added volatility given the Fed is on hold as the government shutdown cancels one jobs report (October) and delays the next (November). The delayed report now comes after the next Fed meeting, meaning the committee won’t have that information to make their interest rate decision. That could reprice the Fed funds futures market for higher rates in the near-term causing added volatility.

The economy is looking more K-shaped with a widening split between the haves and the have -nots. The upper part of the K is driven by the upper class through significant consumer spending. They can support that spending because of the wealth eƯect from their investments. This segment of the population is the primary cause of inflation being sustained at 3.0% when the Fed target is 2.0%.

The lower part of the K is the struggling lower and middle classes. They are having a harder time making ends meet as expenses rise faster than earnings. The weakening labor market, while mild, is causing wage growth to slow. Higher interest rates are also weighing on this segment of the population.

The Fed will need to decide on reducing inflation (i.e. keeping rates higher), thereby hurting the lower K, or reducing rates and supporting the labor market and the lower income earners.

I do think they will ultimately choose to cut rates and support the labor market. This could keep inflation slightly elevated for the time being. The investment implications remain a debasement trade strategy hedging against inflationary pressures. This means owning high-quality stocks of fast-growing companies, hard metals, and even cryptocurrencies.

We are currently taking advantage of some dislocations in the market and continue to add new structured notes to ‘lock in the gains ‘of the last few years while being able to participate in the upside.

As always, we appreciate the trust you place in us and standby for any questions you may have.

Happy Thanksgiving!

Mark J. Asaro, CFA

Author