Client Memo: History Shows Geopolitical Risk is Short-Lived

Mar 12, 2026We are now ten days into Operation Epic Fury, and global financial markets have been rocked by a period of acute volatility. This is that exogenous shock that I described was the real risk to financial markets – more so than high valuations or a recession. The recent volatility is not a function of the prospect of a prolonged war but of fears around prolonged high oil prices.

A sharp rise in oil prices – a key input into nearly everything we do or buy – historically has impacted markets based on two factors: the speed of the increase and its duration. Today, stocks are exhibiting a near-perfect inverse correlation with oil (i.e. oil prices up, stocks down). The price of crude recently topped $100 per barrel. It was just over $60 at the start of the year.

This makes intuitive sense as rising energy costs flow directly to higher input costs and put pressures on margins. Stocks are typically valued by discounting future cash flows back to the present. These higher prices hit those cash flows twofold: 1) as noted, they reduce margins and thus, cash flow, and 2) it boosts inflation expectation by putting upward pressure on inflation and interest rates, reducing the present value of future cash flows.

Right now, the Strait of Hormuz is shut. This is the world’s most important chokepoint for energy with about 21M barrels per day of crude oil and equivalents passing through the waterway. This is about 20% of all global oil consumption. The vast majority of this oil heads to Asia (China, India, South Korea, and Japan).

The result has been a surge in oil prices. While the US is a net oil exporter, crude oil is a worldwide commodity. A hit to supply on the other side of the planet will affect prices here as well. However, you won’t see the same reaction as in Europe or Asia. Gasoline prices are *only* up 18 cents even though crude is up far more.

Markets at this point are gauging the duration and economic impact of the conflict. A significant number of domestic wells were drilled when oil prices were much higher, and at current levels, they become economic to turn back on. As such, additional supply is available domestically and will come online the longer prices remain elevated. As they say, the cure for high oil prices is high oil prices.

The question becomes, who will blink first. At any moment we could have President Trump simply declare victory. Oil prices would likely collapse instantly; but not necessarily return to the pre-conflict levels.

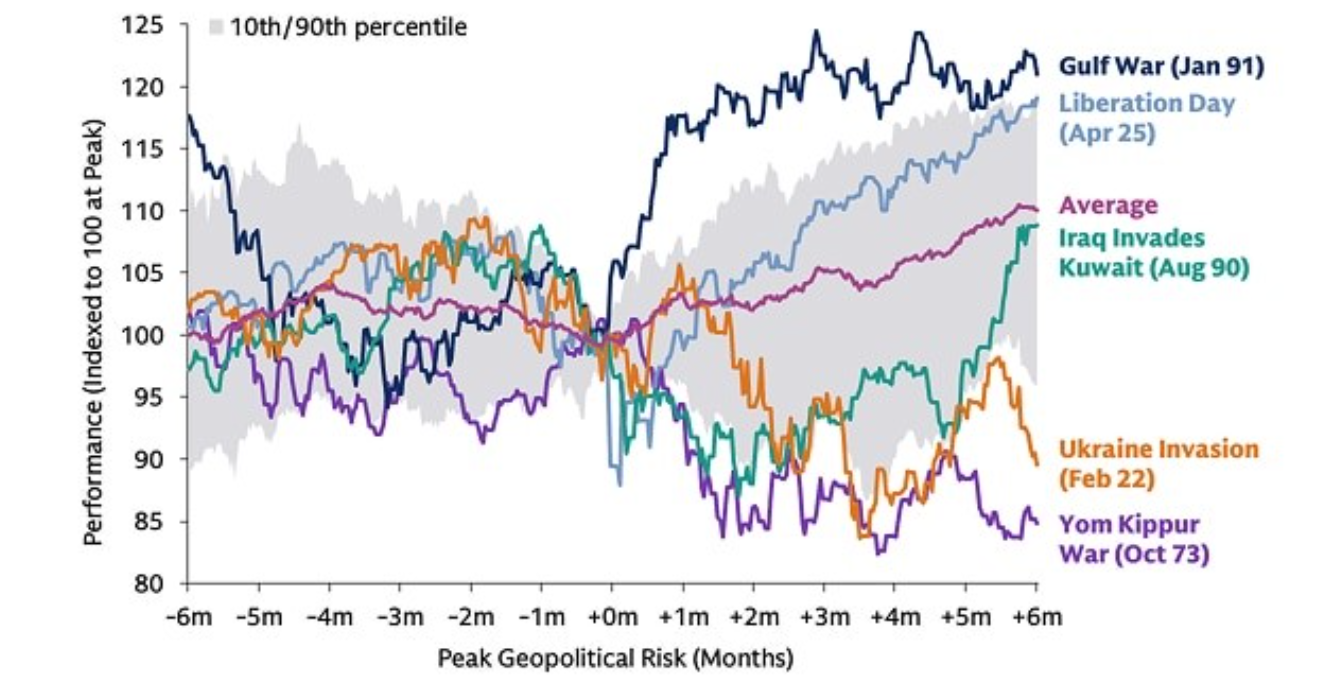

Geopolitical events happen with relative frequency but also tend to end quickly. In the past, they have been historically ideal buying opportunities.

Recall that the price of oil was over $130 at the start of the Russia-Ukraine War, about 30% above the level it is at today. It was also a negative $37 per barrel during Covid, so it can be volatile.

History is crowded with a library of geopolitical shocks. One such data point that is making the rounds is from Ned Davis Research which showed that since 1907 there have been 59 major crisis events. The patterns are all very similar where markets panic at the onset – headlines and uncertainty can definitely be unsettling – and recover over time.

The data shows that the average market decline is about 7%, only to recover those losses within a few months as the immediate reaction and uncertainty passed. In the ten days since the Iran conflict started and markets are down anywhere from 3% to 6%.

Fear and emotions can be problematic, especially in wars. I don’t foresee this conflict lasting all that long. President Trump cares about the stock market and the price of gasoline at the pumps. He’s made it a centerpiece of his economic report card. So, there’s a real incentive for him to find a face-saving short-term solution and declare victory.

We continue to remain invested, making tactical changes to exploit opportunities, and will harvest losses where appropriate.

We stand by if you have any questions or concerns.

Sincerely,

Mark J Asaro, CFA

Noble Wealth Management

Author