Fitch States the Obvious: Implications for the US Debt Being Downgraded

Aug 04, 2023Time to worry. Just kidding.

On August 2nd, Fitch Ratings, one of the nationally recognized statistical ratings organizations, or NRSRO, downgraded the U.S. credit rating one notch to the second highest rating. Fitch is one of the ten approved by the SEC to provide an assessment of the creditworthiness of a firm or financial institution, or sovereign borrower.

While there are ten approved, only three are “major” credit ratings agencies (the other two are S&P Global and Moody’s along with Fitch). So one of the major’s downgrading US debt is a big deal.

Bottom line first: The downgrade is mainly due to the large increase in national public debt and is an assessment of the United States’ longer-term fiscal challenges, not anything new. The downgrade should have little direct impact on financial markets as it is unlikely there are major holders of Treasury securities who would be forced to sell based on the ratings change.

What’s behind the downgrade?

Fitch downgraded the sovereign rating of the US to AA+, from AAA. They cite “the expected fiscal deterioration over the next three years, a high and growing general government debt burden, and the erosion of governance relative to 'AA' and 'AAA' rated peers” as reasons for the downgrade.

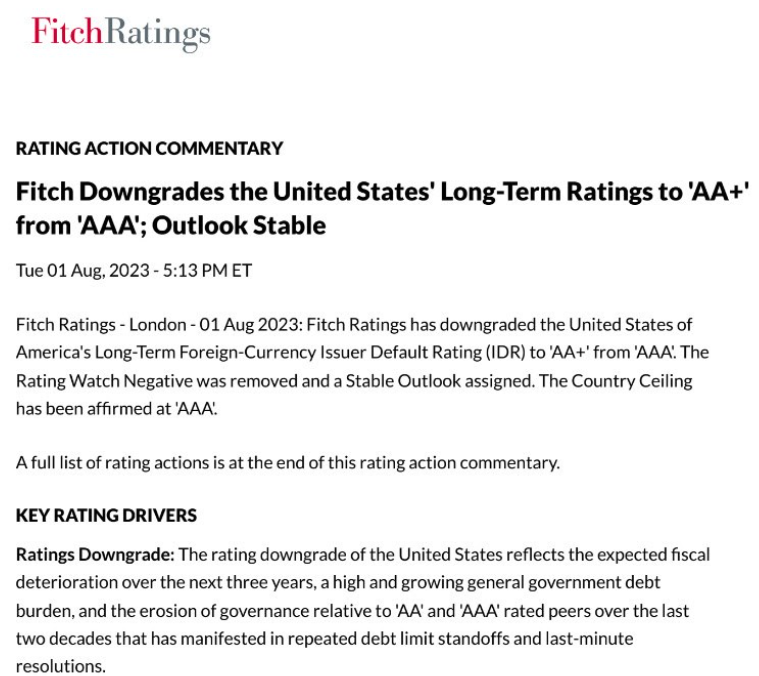

The release from Fitch is below:

Source: Fitch Ratings, Rating Action Commentary, 08/01/2023. Image shows a quote stated by Fitch Ratings.

Again, there is not some new catalyst that triggered the downgrade. They cite in the release that rising general government deficits are expected over the next few years of over 6% of GDPs. GDP last year was over $26.5T so 6% of that is a big number ($1.6T). The US debt load is set to rise by $5.2B every DAY for the next 10 years.

We expect the general government (GG) deficit to rise to 6.3% of GDP in 2023, from 3.7% in 2022, reflecting cyclically weaker federal revenues, new spending initiatives and a higher interest burden. Fitch forecasts a GG deficit of 6.6% of GDP in 2024 and a further widening to 6.9% of GDP in 2025. The larger deficits will be driven by weak 2024 GDP growth.

Essentially, our fiscal house is in disorder. Over the next decade, public federal debt is set to explode higher on healthcare expenses and higher interest burden. Fitch cites CBO projections in its medium-term outlook that projects interest costs will double by 2033 to 3.6% of GDP.

I would note that Fitch did not adjust its “country ceiling”, which it affirmed at AAA. If Fitch had also lowered the country ceiling, it could have had negative implications for other AAA-rated securities issued by US entities. This rating action does not appear to have any implications for securities issued by government-sponsored entities (GSEs), nor for municipal issuers.

Should you be worried? Here are the things that concern me.

- Higher interest rates and a declining dollar. While the dollar will not lose its status as the world’s reserve currency it is likely to be under pressure. That means higher inflation (as import costs rise). The Fed will have to combat that with higher interest rates.

- Potential government shutdown. This gives some ammo to the fiscal hawks in congress to shutting down the government during the next debt ceiling debate. That won’t be until January 2025. However, we do have a budget approval due by September 30th. With the government’s debt burden in such acute focus, spending disputes across and within party lines seem likely. This means that the possibility of a government shutdown can’t be ignored.

- Long-term fiscal challenges are being ignored. Most of us know that the government cannot keep borrowing indefinitely. Now, the government never pays off its debt, it just rolls it when it becomes due. So, the debt continuously builds. Interest payments, thanks to higher interest rates, are skyrocketing. In 2023, the US will pay $663B in interest payments on the national debt, up $476B from last year.

What doesn’t concern me.

- Default. The government still generates a significant amount of tax revenues (and rising) to service the debt. We don’t have a revenue problem. We have a spending problem. The US could easily cut spending if we had the will and be in a strong fiscal position.

- The economy and markets. I’m not worried about ‘China selling our debt’ or anything like that as our economy and markets remain resilient. Other countries own approximately $7.6T of US debt, out of more than $33T. China holds about $869B. It’s not insignificant but selling it would hurt them more than it would harm us.

- The downgrade itself. This is not the first time the US has been downgraded. In 2011, S&P downgraded US debt to the same level that Fitch just did, 13 years later. After that move, interest rates actually fell and the political answer was ‘sequestration.’ At the time, it was billed as a horror but it turned out to be a big success.

Source: Pew Research Center. Data as of 08/04/2023. Graph illustrating U.S. national debt by fiscal year.

Takeaways

The solution to this problem is restraining spending. It’s a hard thing to do. I know from the industry I am in that household’s reducing their spending can be extremely difficult. Once you are used to a specific (and higher) standard of living it is hard to go back.

As someone once said, “I’ve been rich, and I’ve been poor. I prefer rich and want to never be poor again.”

We understand that you might be nervous. While this week’s news flow doesn’t change our outlook for the next year, it can help to remember your long-term investment plan. Uncertainty and volatility can make navigating the market difficult. But over time, diversified income-based portfolios have been able to smooth the ride, especially through the bad stuff.

Sincerely,

Mark J Asaro, CFA

Author